|

In this update...

- Articles & Podcasts

- Sponsor News

- Premium Chart 1

- Premium Chart 2

Articles & Podcasts...

Why Precious Metals Need Equity Market Weakness

Read why we believe that precious metals cannot rebound if the stock market advances. Historically, quite often Gold will bottom as the S&P 500 tops. Also, the gold bugs have lost money and new money is needed to kick-start the renewal of the bull market. That money will slowly come in as the stock market shows more weakness.

Podcast: Sean Brodrick Talks Gold, Miners, Sentiment & Pipelines

My friend Sean Brodrick recently returned from a long trip in Nevada. He toured numerous projects. Hear his view on various topics.

Podcast: Corvus Gold Reports More Great Results from Yellow Jacket

Jeff Pontius discusses the company's latest result from Yellow Jacket, which was one of its best holes ever. Jeff also talks about what the majors are doing and looking for. Despite the renewed downturn in mining stocks, Corvus shares are holding well over $1. In fact, of the 30-40 companies we track (plus the HUI) its one of only two that is trading above a rising 400-day moving average.

Market Breadth Worries

Tiho Brkan notes the growing negative divergences in the US equity market. Four and a half years into a cyclical rebound, these are not the types of things you want to ignore.

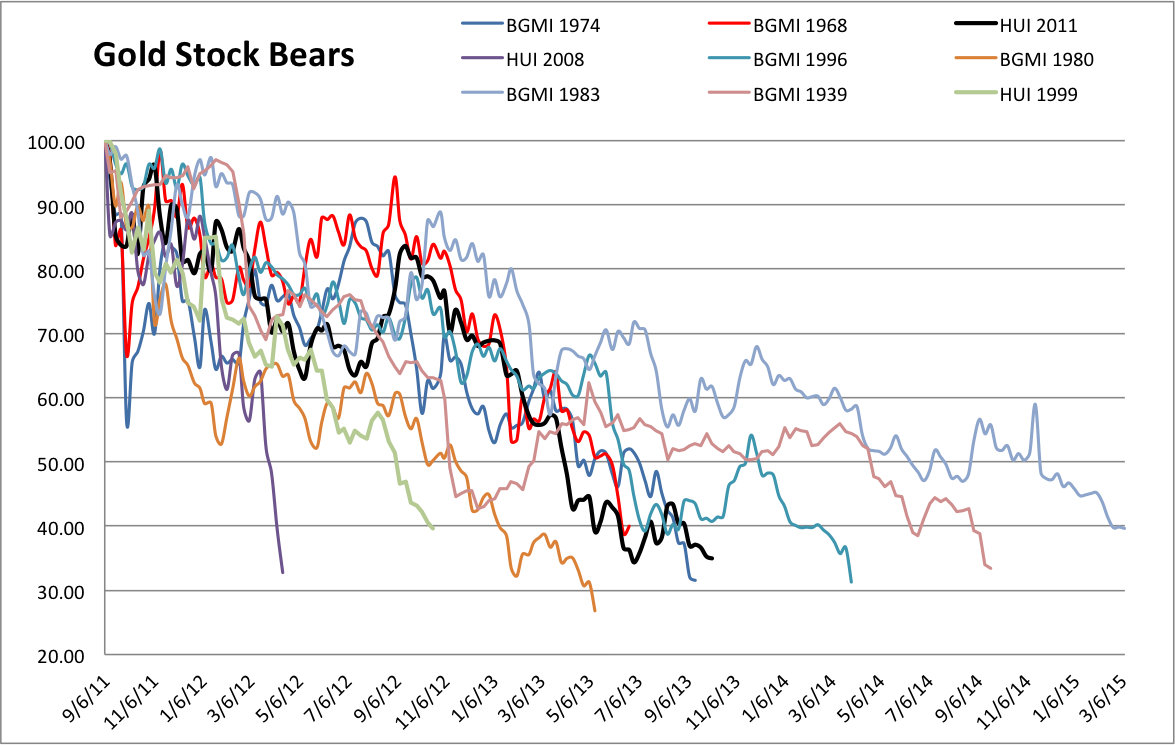

Premium Chart 1

This is an updated look at all the cyclical bear markets in gold stocks. Other than the 1980-1982 bear market, which followed the 1980 bubble and a 20-year bull market, no bear has declined more than 70%. The average is about 68%. The current bear is in black and remains extremely close in price and time to both the 1968 and 1974 bears. This chart cannot predict the exact bottom but it tells us that downside potential from here is extremely limited. Need we mention the 500%-600% moves following the two aforementioned bears?

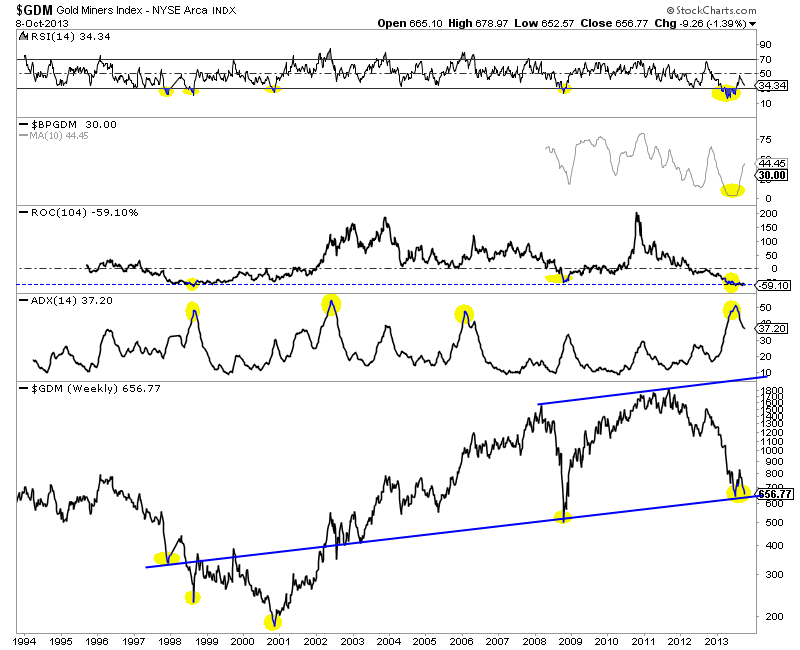

Premium Chart 2

This chart shows GDM which dates back about 20-years. The GDX ETF is constructed from the GDM index. At the summer low there was a record oversold condition in the RSI indicator as well as the Rate of Change indicator. The breadth indicator, BPGDM was at 0%. Though GDM is very close to testing that summer low we now find the RSI and BPGDM indicators in a stronger position. This is what happens as the bottoming process plays out.

Premium Service Notes:

In recent weeks we've updated three major reports for premium subscribers. These include:

- Top 2 Long-Term Speculations (11 pages)

Two speculations which we think can rise 10-20 fold in the coming years

- Top 5 Growth Oriented Producers Report (25 pages)

Reports on our 5 favorite GOPs, all in one file

- Macro Market Update Report (49 pages)

This update examines the outlook for Equities, Commodities, Bonds and Emerging Markets. For the average investor I think this is our most invaluable piece of work (and I intended it to be).

Upon signup, we send you these reports as well as several other reports (Rules Report, Criteria Report for Producers/Explorers) and all recent updates. Not only do you get all of these reports sent to you immediately but you get all of our regular updates for 6 months. Our subscribers are my lifeblood. It is a pleasure to do the work we do. Huge profits are coming in the coming months, quarters and years and we want to help everyone attain huge profits.

Wishing you good health and profits,

-Jordan

Disclaimer: Sponsor Companies are paid sponsor companies of TheDailyGold.com website and this free newsletter. Do not construe sponsorship with a recommendation. The author of this newsletter is not a registered investment advisor. This newsletter is intended for informational and educational purposes only and should not be considered personalized and individualized investment advice. Investment in the precious metals sector contains significant risks. You should consult with an investment advisor and due your own due diligence. This email may contain certain forward looking statements which are subject to risks, uncertainties and a multitude of factors that can cause results and outcomes to differ materially from those discussed herein.

|

|